- Even when glut stops growing, market might shrug: SocGen

- History shows oil rebound will hinge on stockpiles: Goldman

Even if Saudi Arabia wins its struggle with U.S. shale producers over market share, it will face a new billion-barrel adversary.

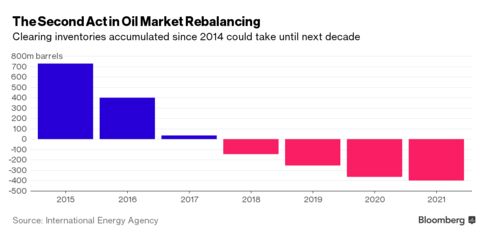

It won’t be regional nemesis Iran, a resurgent Iraq or long-standing competitor Russia. The answer will be more prosaic: Even when overproduction ends, a stockpile surplus of more than 1 billion barrels built up since 2014 will remain, weighing on prices. Inventories will keep accumulating until the end of 2017, the International Energy Agency forecasts, and clearing the glut could take years.

“We may get to the end of the year, and even though supply and demand are in balance, the market shrugs and says ‘So what?’ because it’s waiting for proof of inventory draw-downs,” said Mike Wittner, head of oil markets at Societe Generale SA in New York. “Moving from stock-builds to balance might not be enough.

Since it was unveiled in late 2014, Saudi Arabia’s strategy to bring the world’s oversupplied oil markets back into balance by squeezing competitors with lower prices has proved grueling, dragging crude down to less than $30 a barrel last month. While a gradual decline in U.S. production signals supply will stop growing, the second act of the process may prove the longest as stockpiles slowly contract.

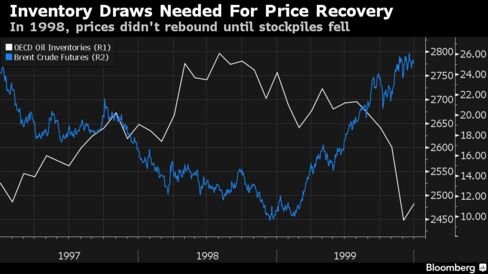

For a historical precedent, Goldman Sachs Group Inc. points to the oil glut that developed in 1998 to 1999 as demand plunged in the wake of the Asian financial crisis. Crude prices kept falling even as the Organization of Petroleum Exporting Countries made output cuts in March and then June of 1998, slipping below $10 a barrel in London in December of that year. It wasn’t until stockpiles in developed economies started dropping in early 1999 that the recovery took shape.

Between late 2014, when developed-world stockpiles were at about average levels, and the end of this year, global inventories will have swelled by about 1.1 billion barrels, IEA data shows. Another 37 million will be added in 2017. Taking the agency’s projections for how quickly inventories will then fall, and estimates from Energy Aspects Ltd. that 290 million barrels will flow into China’s strategic reserves, it will take until 2021 to clear what’s accumulated.

The latest data from the American Petroleum Institute show the build-up in the U.S. is only getting bigger, with the nation’s crude stockpiles ballooning by 9.9 million barrels last week. West Texas Intermediate crude futures were little changed at $34.38 a barrel at 12:03 p.m. in New York.

“For the previous eight quarters to this one, we have had global implied stock-builds, so we have accumulated a lot of oil,” said Harry Tchilinguirian, head of commodity markets strategy at BNP Paribas SA in London. “It’s going to take a lot of time to work out that excess oil from the system.”

Missing Barrels

Inventories could erode as early as this summer because the decline in U.S. shale output will probably be steeper than is widely assumed, according to Vienna-based consultants JBC Energy GmbH, which predicts prices could rebound to $50 a barrel in June. Much of the surplus the IEA estimates accumulated in the fourth quarter of 2015 hasn’t actually appeared in storage, suggesting the excess is smaller than thought, Standard Chartered Plc says.

“The most likely explanation for the majority of the missing barrels is simply that they do not exist” and are the “result of underestimation of demand and overestimation of supply,” said Paul Horsnell, head of commodities research at Standard Chartered. “They imply that the global market will swing back into deficit well before consensus.”

Saudi Arabia repeated last week that it won’t speed up the re-balancing process by reducing its own supply. While the kingdom and some other OPEC members have agreed with Russia to freeze output at January levels, a coordinated cut is “not happening,” Saudi Oil Minister Ali al-Naimi said at the IHS CERAWeek conference in Houston on Feb. 23.

Inventories started to swell in 2014 as the wave of supply unleashed by the U.S. shale oil boom, coupled with other new output, outpaced growth in global oil demand by a factor of three. The pile-up continued in 2015 as OPEC members like Saudi Arabia and Iraq raised production to defend their share of world markets. Tanks are poised to fill even more as Iran -- freed as of last month from international sanctions -- pushes new exports into a market that’s already saturated.

The time it will take to use up what’s sitting in tanks around the world adds to Goldman Sachs’s confidence in its prediction, by now an oil-industry mantra, that prices will stay “lower for longer.”

“The market will have a hard time trading higher once supply and demand shift into a deficit as the inventory overhang will likely act as a drag until stock levels are normalized,” said Jeff Currie, head of commodities research at Goldman Sachs in New York.

No comments:

Post a Comment