- Justin Trudeau: My Father Gave Me Values, Principles

- Canadian leader says he will be `responsible' with deficits

- New Liberal prime minister prefers longer-term investments

Canada Prime Minister Justin Trudeau sought to reassure Wall Street investors he’ll remain cautious on spending as he prepares to push the nation deeper into deficit, distancing himself from another deficit-spending leader: his father Pierre.

Trudeau says his new Liberal government isn’t looking to flood the economy with money now beyond what was promised in last year’s election campaign, saying he needs to be responsible and keep the budget gap under control.

“What we’re looking at is not so much trying to jolt the economy into life as trying to lay the groundwork, the foundation, for better growth, better productivity, over the long term,” Trudeau said in an interview Thursday with Bloomberg Editor-in-Chief John Micklethwait. This is “not just an instant influx of cash.”

Trudeau, on his first visit to New York since winning office in October, is trying to keep the nation’s lenders on board with his plans to kick start the economy with deficit spending that some economists predict will run as high as C$150 billion ($115 billion) over the next five years. To assuage them, Trudeau is telling investors the money will be well spent.

The prime minister’s comments to a room full of Wall Street investors at Bloomberg’s headquarters come ahead of his first budget on March 22, which is said to include a projected deficit of about C$30 billion for the fiscal year beginning April 1. The bulk of that reflects the impact of a worsening economic outlook as plunging oil prices push the energy hub of Alberta into recession. The Liberals have also indicated they will carry out campaign pledges worth C$10.5 billion.

Fiscal Jolt

Some economists have called for even more spending to stoke Canada’s sluggish growth. The Bank of Canada has said it held off from cutting interest rates in part to account for the increased government stimulus.

Avery Shenfeld, chief economist at CIBC World Markets in Toronto, said he estimates government spending will add 0.5 percentage points to growth this year, assuming a deficit of C$40 billion. Trudeau “does sound a bit more cautious,” Shenfeld said from Toronto after Trudeau spoke.

Trudeau’s remarks “provide some confirmation of the view that any boost to growth this year is likely to be small in scale,” Brian DePratto, an economist at Toronto-Dominion Bank said in a telephone interview.

Canada’s benchmark stock index and its currency rose Thursday as oil and metal prices rebounded. The Standard & Poor’s/TSX Composite Index rose 1.2 percent. The loonie, as the currency is called, soared to a five-month high of 76.91 U.S. cents.

Sparking Growth

Trudeau said there’s no need for stimulus on the scale of the 2008-09 recession that was carried out by his Conservative predecessor, Stephen Harper.

“One of the things that’s really important to me is fiscal responsibility,” Trudeau said. “Quite frankly we feel that what we’ve put forward is what the economy can absorb as a way of creating the long-term growth.”

Trudeau called Thursday for other Western leaders to shy away from austerity and invest now. In the wide-ranging interview, he praised struggling aircraft manufacturer Bombardier Inc.’s “fabulous” C Series jet while ducking questions of whether his government will agree to provide aid to the company.

Currency and Carbon

He said he’s comfortable with the Canadian dollar, which sunk quickly in his first few months in office amid the commodities slump yet has since rebounded. After reaching parity with the U.S. dollar three years ago, the currency declined an unprecedented 25 percent, touching a 13-year low at the beginning of the year. It has rallied 11 percent since Jan. 20.

The prime minister said he will be “ruthless” in cutting carbon emissions, adding that doing so can offer Canada economic opportunities as a leader in green technology.

Ahead of his looming budget, Trudeau’s fiscal policy is under close watch. Trudeau won power as the sole party leader to pitch deficits to voters. On the day he made that pledge, he said he went home and told his wife Sophie he was convinced he was going to win the election, even though he began the campaign in third place.

“The next morning she opened up the newspaper and she said, ‘Well, it doesn’t say anything about that, but you just won the election?’,” he explained. “And I said, ‘Now, it’s going to take a while for people to figure it out.’”

Taking Office

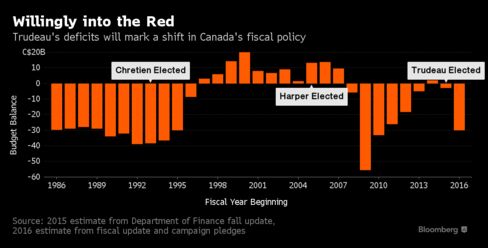

Since the election, the fiscal outlook has worsened, with Trudeau now on pace to run a deficit triple what he had promised in the campaign.

The prime minister was careful Thursday to distance himself from his father’s record of soaring debts and deficits during the oil and inflation crisis of the 1970s. The senior Trudeau ran up C$187 billion in total deficits, averaging 3.7 percent of gross domestic product between 1968 and 1984, unprecedented levels at that time in a non-war era. That’s more than twice as high as Canada’s projected deficit for this fiscal year.

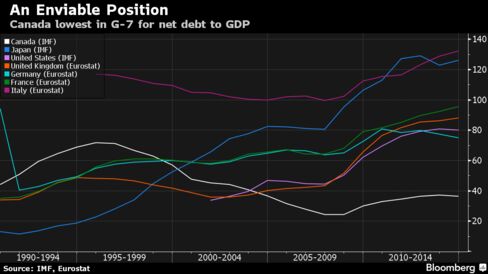

Canada’s aversion to debt was cemented in the mid-1990s amid rating downgrades, a falling currency and a national unity crisis. Canada lost its coveted AAA rating from Moody’s Investors Service Inc. in 1994 on concern the country would have trouble repaying its debt, which at the time was the second-highest among G-7 countries after Italy. It took seven years to win it back, giving Trudeau the wiggle room to run deficits now.

“Trying to compare the economic circumstances on a global scale in the 1970s to what we’re going through now is very different,” Trudeau said. “I come at it with a different perspective from my father.”

“Certainly the solutions I’m putting forward are not based in nostalgia,” he said.

Activist Tilt

Like his father, Trudeau, 44, is boosting the role of the state and has moved quickly to reduce income inequalities. He has raised taxes on incomes above C$200,000, cut them for middle-income earners and will unveil in his budget a substantial new Canada Child Benefit program that will direct billions in payments to families with children.

Trudeau has also pledged C$60 billion in new infrastructure funding over 10 years, with C$5 billion expected in each of the next two fiscal years. To ensure responsible spending, the big projects will wait.

“I think the challenge when you shovel money out the door is it doesn’t always get spent on the right things,” Trudeau said. “The first two years, we’re going to do the unsexy things that governments hate to announce -- recapitalization of infrastructure, maintenance, upgrades, the things you don’t get to cut a ribbon or announce a shiny new building on.”

No comments:

Post a Comment